Why Legal Advice Is the Ultimate Risk Control Move

Most people think legal consultation is only for lawsuits or contracts. I used to believe that—until I nearly lost everything over a tax oversight. That wake-up call taught me the hard way: smart risk control isn’t just about investments, it’s about protection. Now, I see legal guidance as a financial strategy, not an expense. Let me share how this shift saved me stress, money, and potential disaster. What started as a simple oversight—a misclassified investment on a tax form—spiraled into months of audits, penalties, and sleepless nights. I had focused so much on growing my portfolio that I ignored the foundation beneath it. Legal advice was something I associated with conflict, not prevention. But now I understand: just as you wouldn’t drive without insurance, you shouldn’t manage wealth without legal insight. It’s not about avoiding problems after they arise—it’s about designing a structure that prevents them in the first place. This is the kind of financial wisdom that doesn’t show up on a balance sheet, but quietly protects everything it represents.

The Hidden Cost of Skipping Legal Advice

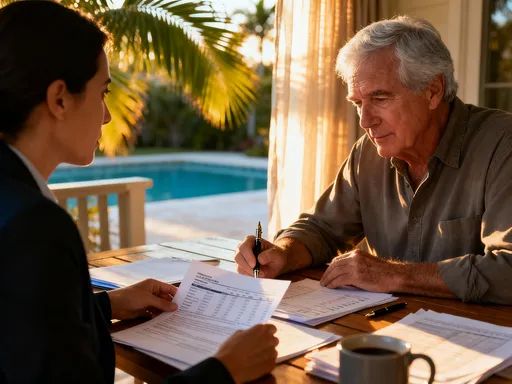

Many people treat legal consultation as a luxury or a last resort, something to call on only when disputes arise or documents need signing. This mindset, however, carries hidden but significant financial risks. The reality is that legal oversights often compound silently, only revealing their damage when it’s too late to reverse. Consider the small business owner who operates as a sole proprietor without forming a legal entity. On the surface, this simplifies operations and reduces paperwork. But in the event of a lawsuit or debt claim, personal assets—homes, savings, vehicles—can be exposed to seizure. This isn’t a rare scenario; it’s a common outcome when legal structure is overlooked.

The financial toll of skipping legal advice often exceeds the cost of the consultation itself. Take the case of an investor who purchases rental property with a family member but fails to formalize ownership shares. Without a clear agreement, disagreements over income distribution, maintenance responsibilities, or sale decisions can escalate into costly litigation. In one documented situation, a co-owner attempted to sell their share without consent, leading to a legal battle that drained over $40,000 in legal fees and stalled the property’s profitability for nearly two years. These aren’t hypotheticals—they reflect real financial losses that could have been avoided with a modest upfront legal investment.

Beyond direct financial loss, the emotional burden of legal crises is often underestimated. Stress, family conflict, and loss of confidence in financial decisions can linger long after the legal issue is resolved. One study by a financial wellness group found that individuals involved in preventable legal disputes reported higher levels of anxiety and lower satisfaction with their financial lives—even when they ultimately won their cases. This underscores a critical point: legal advice is not just about compliance or dispute resolution. It’s a form of financial insurance. Just as homeowners insurance protects against fire or theft, legal consultation protects against structural vulnerabilities in your financial life. The cost of a consultation may range from a few hundred to a few thousand dollars, but it can prevent losses worth ten or even a hundred times that amount.

Moreover, many financial decisions—such as gifting assets, starting a side business, or refinancing property—trigger legal implications that aren’t immediately obvious. Without guidance, individuals may unknowingly violate tax codes, breach fiduciary duties, or create enforceable obligations they didn’t intend. The absence of legal review doesn’t eliminate risk; it simply defers it, often to a time of personal or economic vulnerability. Recognizing this hidden cost is the first step toward smarter financial stewardship. Legal advice, when used proactively, shifts the financial paradigm from reactive damage control to strategic prevention.

Legal Consultation as a Strategic Shield, Not a Reactive Fix

The traditional view of legal services positions them as a response to problems—lawyers are called when disputes arise, contracts are breached, or audits begin. But this reactive model fails to capture the true value of legal insight. When integrated early and consistently, legal consultation functions as a strategic shield, helping individuals and families avoid exposure before it occurs. This proactive approach transforms legal advice from a cost into an investment—one that strengthens the foundation of every financial decision.

Consider the process of starting a small business. Many entrepreneurs begin operations without formalizing their business structure, assuming that revenue and customer growth are the only priorities. However, the choice between a sole proprietorship, partnership, LLC, or corporation has profound legal and financial consequences. An LLC, for example, provides liability protection that separates personal assets from business risks. Forming this entity early, with proper legal guidance, can prevent a single lawsuit from threatening a family’s home or savings. The cost of formation—typically a few hundred dollars—is minimal compared to the potential loss.

Similarly, in estate planning, legal foresight can prevent family conflict and administrative delays. A well-drafted will, supported by trusts and powers of attorney, ensures that assets are transferred according to the individual’s wishes. Without these documents, state laws determine inheritance, which may not align with the family’s intentions. In one case, a widowed mother passed away without a will, leaving her estate to be divided among surviving children. One sibling, who had cared for her for years, received the same share as others who had been absent. This led to resentment and a breakdown in family relationships—emotional costs that no amount of money could repair. Legal consultation in this context isn’t about complexity; it’s about clarity and peace of mind.

Another powerful example is in real estate investing. Purchasing property in a personal name versus a holding company affects liability, tax treatment, and financing options. A legal advisor can help structure the transaction to minimize risk and maximize flexibility. For instance, placing rental properties in a limited liability company can shield other assets if a tenant sues for injury. It also simplifies management and can provide tax advantages when properly aligned with accounting strategies. These decisions are not one-time events; they create long-term frameworks that influence financial outcomes for years.

The strategic value of legal consultation extends beyond individual decisions to overall financial resilience. Just as a well-diversified portfolio reduces investment risk, a legally sound structure reduces life risk. This doesn’t mean consulting a lawyer for every minor decision. Rather, it means establishing a relationship with a trusted advisor who understands your financial landscape and can flag potential issues before they arise. In this role, legal counsel becomes a partner in financial planning, not just a troubleshooter. The shift from reactive to proactive is subtle but transformative—one that turns legal advice into a cornerstone of sustainable wealth.

Tax Risks You’re Probably Ignoring (And How Legal Counsel Catches Them)

Tax efficiency is a key driver of long-term financial success, yet many individuals expose themselves to unnecessary risks by managing tax strategy without legal oversight. While accountants and tax software play vital roles, they are not substitutes for legal expertise—especially when transactions cross jurisdictional lines, involve complex ownership structures, or include international elements. Legal counsel brings a layer of precision that prevents costly missteps and ensures compliance with evolving regulations.

One common pitfall is the misclassification of income. For example, an individual who earns rental income may treat it as passive revenue without realizing that active management could reclassify it as business income, triggering self-employment taxes. Similarly, digital entrepreneurs who sell online courses or subscriptions may not recognize that their activities constitute a formal business, requiring registration, licensing, and proper tax reporting. Without legal guidance, these oversights go unnoticed until an audit reveals them, often resulting in penalties, interest, and back taxes.

Another area of risk involves deductions. While the tax code allows for numerous deductions, the rules governing eligibility are strict. Home office deductions, vehicle expenses, and business travel must be documented with accuracy and supported by legal standards. Claiming deductions without proper substantiation can lead to disallowance and penalties. A legal advisor can help structure these claims within safe harbor rules and ensure that recordkeeping meets audit standards. This is especially important for self-employed individuals and small business owners, who are more likely to be scrutinized by tax authorities.

Cross-border transactions introduce even greater complexity. A retiree who receives pension income from another country, for instance, may be subject to reporting requirements under the Foreign Account Tax Compliance Act (FATCA). Failure to file required disclosures, such as the FBAR (Report of Foreign Bank and Financial Accounts), can result in penalties exceeding $10,000 per violation. Legal counsel familiar with international tax law can help navigate these requirements, ensuring compliance while avoiding double taxation through treaties and credits.

Additionally, legal advisors can identify opportunities for tax optimization that go beyond simple deduction maximization. For example, they can recommend entity structures that reduce tax liability, such as using an S-corporation for a small business to separate salary from distributions. They can also advise on timing strategies—such as when to realize capital gains or convert traditional IRAs to Roth accounts—based on current tax brackets and future projections. These strategies require a deep understanding of both tax law and personal financial goals, making legal consultation an essential component of comprehensive planning.

The contrast between DIY tax management and expert-informed strategy is stark. While tax software can process forms efficiently, it cannot interpret the nuances of individual circumstances or anticipate regulatory changes. Legal counsel, on the other hand, provides context-aware guidance that balances risk and reward. This doesn’t mean eliminating personal responsibility; it means making informed decisions with professional support. In an environment where tax laws change frequently and enforcement is increasing, legal advice is not an optional add-on—it’s a necessary safeguard.

Asset Protection: Building Walls Around Your Wealth

Wealth accumulation is only half the financial equation; the other half is preservation. No matter how successful an investment strategy may be, its value can be erased overnight by a single legal judgment or liability claim. This is where asset protection comes in—a proactive approach to shielding wealth from unforeseen threats. Legal consultation plays a central role in designing these protective structures, ensuring that assets are not only grown but also defended.

One of the most effective tools for asset protection is the trust. Unlike a will, which only takes effect after death, a trust can operate during an individual’s lifetime and provide ongoing management of assets. Revocable living trusts, for example, allow the grantor to retain control while avoiding probate—a lengthy and public legal process. Irrevocable trusts go further by removing assets from the individual’s estate, protecting them from creditors and reducing estate tax exposure. These structures are not just for the wealthy; they can benefit anyone with significant assets, such as a home, retirement accounts, or investment portfolios.

Ownership titling is another critical factor. How an asset is titled—jointly, individually, or through an entity—determines who has legal claim to it and under what circumstances. For instance, holding real estate in joint tenancy with rights of survivorship ensures automatic transfer to the surviving owner, bypassing probate. But in some cases, this can create unintended tax or liability consequences. A legal advisor can help choose the optimal titling method based on estate goals, tax implications, and risk exposure.

Liability separation is equally important, especially for individuals with high exposure due to their profession or lifestyle. Doctors, contractors, and business owners face greater risk of lawsuits, making legal structuring essential. Forming a limited liability company (LLC) or a professional corporation (PC) creates a legal barrier between personal and business assets. As long as the entity is properly maintained—keeping separate bank accounts, records, and avoiding commingling of funds—the owner’s personal wealth remains protected.

Consider the case of a freelance consultant who operates without an entity. After delivering a project, a client claims the work caused financial loss and files a lawsuit seeking damages. Without liability protection, the consultant’s personal savings and home could be at risk. But if the same work had been conducted through an LLC, only the business assets would be exposed. This distinction can mean the difference between a manageable legal defense and financial ruin.

Asset protection is not about hiding wealth or evading responsibility. It’s about responsible stewardship—using legal tools to ensure that wealth serves its intended purpose: security, legacy, and peace of mind. Legal consultation ensures that these structures are implemented correctly, avoiding technical flaws that could invalidate protections. When done right, asset protection is not a reactive defense but a proactive design—one that aligns with long-term financial goals and values.

Contracts That Work for You—Not Against You

Contracts govern nearly every financial transaction—real estate purchases, business partnerships, service agreements, and investment deals. Yet many people sign them without review, assuming that standard forms are fair or that verbal agreements are sufficient. This assumption can lead to serious consequences. A contract is not just a formality; it is a binding legal document that defines rights, responsibilities, and remedies. Without proper scrutiny, it can contain clauses that undermine financial interests or expose individuals to unexpected obligations.

One of the most common issues is ambiguous language. Phrases like “reasonable efforts,” “best practices,” or “as soon as possible” may sound cooperative but lack legal precision. In a dispute, these terms are open to interpretation, often favoring the party with greater resources or legal representation. A legal advisor can clarify such language, ensuring that expectations are defined and enforceable. For example, in a service agreement, specifying exact delivery dates, performance metrics, and termination conditions protects both parties and reduces the risk of conflict.

Another risk lies in one-sided clauses. Many standard contracts—especially those drafted by the other party—include provisions that disproportionately favor the drafter. These may include automatic renewals, unlimited liability, or mandatory arbitration in a distant jurisdiction. A legal review can identify these imbalances and negotiate more equitable terms. In a real estate lease, for instance, a tenant might unknowingly agree to a clause allowing the landlord to increase rent by any amount with 30 days’ notice. A legal advisor can amend this to include caps or indexing, providing stability and predictability.

Partnership agreements are particularly vulnerable to oversight. When friends or family members start a business together, they often rely on trust rather than written terms. But without a formal agreement, disagreements over profit sharing, decision-making authority, or exit strategies can escalate into legal battles. A well-drafted partnership agreement outlines roles, responsibilities, capital contributions, and dispute resolution mechanisms. It may also include buy-sell provisions that specify how ownership interests are transferred if a partner leaves or passes away. These details prevent emotional conflicts from turning into financial disasters.

The value of legal review is not limited to complex deals. Even simple agreements, such as a promissory note for a personal loan, benefit from professional input. Without proper documentation, a loan may be treated as a gift for tax purposes, triggering gift tax implications. A legally sound note includes repayment terms, interest rate (if any), and default provisions, ensuring enforceability and clarity. In all cases, the goal is not to create adversarial relationships but to establish clear, fair, and enforceable terms that protect everyone involved.

Navigating Regulatory Shifts Without Panic

Financial regulations are not static. Tax codes, reporting requirements, and compliance standards evolve in response to economic conditions, technological changes, and policy shifts. For individuals and business owners, keeping up with these changes can be overwhelming. Yet falling behind can lead to penalties, audits, or loss of eligibility for benefits. This is where ongoing legal consultation provides critical value—not as a one-time fix, but as a continuous monitoring system that ensures adaptability and compliance.

Recent years have seen significant regulatory changes. The introduction of the SECURE Act, for example, altered retirement account rules, affecting required minimum distributions and inheritance planning. Similarly, the Inflation Reduction Act included new tax credits for energy-efficient home improvements, but with specific eligibility criteria. Without legal guidance, individuals may miss opportunities or inadvertently violate new rules. A legal advisor stays informed about these developments and helps clients adjust their strategies accordingly.

For business owners, compliance is even more complex. Employment laws, data privacy regulations, and industry-specific standards require constant attention. A small business that collects customer data, for instance, may be subject to state-level privacy laws like the California Consumer Privacy Act (CCPA). Failure to implement proper data handling procedures can result in fines and reputational damage. Legal counsel can conduct compliance reviews, update policies, and train staff, reducing exposure to regulatory risk.

The benefit of ongoing legal oversight is not just compliance—it’s confidence. When laws change, individuals with legal support can respond calmly, knowing their advisor is monitoring the landscape. This prevents reactive decision-making based on fear or misinformation. Instead, adjustments are made strategically, with full understanding of implications. In uncertain economic times, this stability is invaluable. Legal consultation becomes a form of risk management, ensuring that financial plans remain resilient in the face of change.

Making Legal Advice Affordable and Actionable

One of the most persistent myths about legal advice is that it’s only for the wealthy. This belief keeps many individuals from seeking help until a crisis occurs. The truth is that legal consultation has become more accessible than ever, with a range of options designed to fit different budgets and needs. The key is to view legal advice not as an expense, but as a high-impact investment in financial security.

Flat-fee services have made legal help more predictable and affordable. Instead of paying by the hour, clients can pay a fixed rate for specific services—such as drafting a will, forming an LLC, or reviewing a contract. This model removes uncertainty and allows for better budgeting. Many law firms now offer tiered packages, providing basic, standard, and premium options based on complexity. For example, a basic estate plan may include a will and power of attorney for a few hundred dollars, while a comprehensive plan with trusts and tax planning costs more but offers greater protection.

Retainer models are another option, particularly for business owners or individuals with ongoing legal needs. By paying a monthly fee, clients gain access to a lawyer for consultations, document reviews, and advice as issues arise. This creates a proactive relationship, reducing the need for emergency interventions. Legal tech platforms have also expanded access, offering online tools for document creation, legal Q&A, and virtual consultations. While these tools don’t replace a lawyer, they can complement professional advice and reduce overall costs.

Additionally, many communities offer low-cost or free legal aid through nonprofit organizations, bar associations, or government programs. These services are especially helpful for basic estate planning, tenant rights, or small business formation. Some financial institutions and credit unions even include legal consultation as part of membership benefits, recognizing its role in financial wellness.

The bottom line is that legal advice doesn’t have to be expensive to be effective. What matters is consistency and timing. A small investment in legal guidance today can prevent a major financial setback tomorrow. It’s not about hiring a lawyer for every decision—it’s about knowing when to seek help and building a relationship with a trusted advisor. In this way, legal consultation becomes an integral part of financial planning, not an afterthought. It’s one of the most effective forms of risk control available, offering protection, clarity, and peace of mind. In the world of personal finance, that’s a return worth every penny.